Latest Posts

Skai Director of Sales joins Podean as Director of Retail Media Partnerships

September 12, 2023

Podean Turkey launches & unveils ecommerce research

August 5, 2022

This article was written by Podean Global CEO Travis Johnson and originally published on The Drum on April 16 2021. Full article can be found here.

Cast your mind back to late 2019. At Podean we were having lots of conversations with big brands telling us that focusing on ecommerce and marketplaces was on their agenda, but not their top priority and not a massive driver of sales.

Then of course Covid hit the world and e-commerce deliveries were the main way many Americans could receive the products they needed in their life. Amazon was a clear beneficiary with 2020 net sales growing to $386b, a 37.6% increase from $281bn in 2019. Many brands (even those late to the party) saw substantial year-on-year ecommerce growth – 40%, 50%, 80% and even 120% growth was not uncommon.

But is the pendulum swinging back?

The growth many brands enjoyed in 2020 is unlikely to be replicated in 2021. Brands currently selling on Amazon are facing five clear challenges:

1. There’s more competition than ever.

It wasn’t just a couple of brands that realized they need to focus on ecommerce and marketplaces during the pandemic, it was hundreds of thousands of new sellers. More competitors means it’s harder to maintain top rankings, and more competition for advertising placements drives higher advertising costs and lower share of voice leading to a lower share of shelf.

Marketplace Pulse suggests there are 9.8 million registered sellers globally and 1.9 million active. They estimate that in 2021 so far 354,000 new sellers have joined the platform – being 3,408 new sellers every day, or 142 every hour, or even 2 every minute. These competitors are also more sophisticated, better prepared and optimized for Amazon. Brands expecting to achieve stratospheric growth on Amazon just by riding the wave are going to be disappointed.

Amazon has also expanded their own retail presence globally, adding Sweden and Saudi Arabia in 2020 and they’re now present in 20 countries. With every new geography Amazon adds they also source and cross-sell products between markets. For example, a product they buy from a local brand in the UK will likely be offered for sale to Swedish customers. So your competition on Amazon isn’t just against other Amazon sellers, it’s exacerbated by Amazon themselves.

2. Margin pressure.

We hear from clients that the vendor negotiations this year have been particularly “robust” with marketplaces (especially Amazon) demanding significantly higher margins and concessions. Co-op marketing fees are increasing, payment terms lengthening and other services such as paying for a Strategic Vendor Services (SVS) manager or merchandising placements are being mandated. Indeed we have heard that Amazon is framing that the only way to even have a full negotiation with them is to pay for SVS services.

Brands also need to leverage their agency relationships and broader knowledge to understand benchmarks for their negotiations. Sometimes a brand may be relying on their own past experience and not aware of other concessions that might be more beneficial to their business.

3. The world (and malls) are opening back up.

Skyfii is a leading provider of wifi and analytics to shopping malls across America and measures foot traffic among other metrics. In January to March 2021 they saw mall traffic rise 45.3% representing millions and millions of extra shoppers buying from bricks-and-mortar retailers. During this same period overall retail sales did not increase by the same percentage, meaning there is a shift to people decreasing their ecommerce spend and buying more items in-person.

4. Consumer uncertainty around the economy.

The latest round of $1400 stimulus checks were delivered starting at the end of March and will flow to most eligible Americans by the end of May 2021. In the weeks leading up we saw retail sales drop off – likely people waiting until the check arrived before spending more.

This was reflected in National retail sales that saw a drop of 3% between January 2021 and February 2021. Online and other non-store sales decreased 5.4%.

March retail data – just released on 15th April – showed the considerable impact of stimulus checks. Retail sales in April jumped 9.8% higher with motor vehicles and parts, sporting goods, clothing and food and beverage leading the gains contributing to the best month for retail since the May 2020 gain of 18.3%, which came after the first round of stimulus checks. US Jobless claims added to the good economic news, with first-time filings for unemployment insurance plunging to 576,000, easily the best week since the beginning of the Covid-19 pandemic.

Suffice to say, these wild monthly swings significantly impact consumers, their spending patterns and makes forecasting for brands quite a challenge.

5. Global logistics are still struggling to keep up.

Ships are stationed off the coastlines around the US and all aspects of receiving and transporting goods are under pressure – in terms of both the timing, and cost, of imports. Many brands are struggling to keep products in stock.

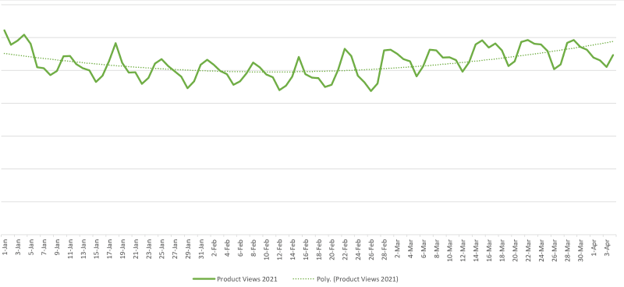

6. Amazon traffic fluctuations.

Using Google Trends as a macro view on people searching for the term “Amazon” we saw a decline of approximately 7% across the first months of 2021.

Using more precise data, SimilarWeb saw a dip in total Amazon views during the February and March months by approximately 10% versus the January starting point. From late March (also likely impacted by stimulus checks) page views look to be trending upwards.

When we look at year-on-year comparisons, SimilarWeb reveals an interesting story.

Between Jan 1st and Mar 31st, year-on-year total Amazon units sold increased +35%, page views increased +32% but revenue only +24% inferring a lower average selling price for brands on the platform.

When looking at some specific categories the data is more pronounced. For example, pet supplies during the same period experienced +43% product views but category sales revenue only increased +15%. For makeup and cosmetics page views were +11% but revenue declined -5%. For computers and laptops pageviews declined -4% and revenue declined -5%

So with all of this data and insight, what should brands do?

- Make sure your presence and performance on marketplaces is as strong as it can be. Brands must ensure their content, creative, retail operations and advertising is all optimized and they are not leaving themselves exposed to competitors stealing market share.

- Keep a close eye on physical store sales and ecommerce sales and be prepared to revise 2021 targets for each sales channel. All indicators are that there will be overall ecommerce growth (but considerably lower than the jump seen 2019 > 2020) and a bounce-back in physical store sales.

- Monitor product-level demand closely. The fluctuating economy, unemployment and stimulus all make for unpredictable times and consumer spending patterns may shift. They may choose more affordable products over more expensive ones.

- Rigorously focus on predicting demand and ensuring your supply chain is as optimized as it can be. Running out of stock doesn’t just inhibit short-term revenues, ecommerce marketplaces will also penalize you for this over the longer term and you’ll likely see your rankings drop and take some time to recover

- Continue to explore the addition of new products, new markets, and new marketplaces to drive sales growth.

This article was written by Podean Global CEO Travis Johnson and originally published on The Drum on April 16 2021. Full article can be found here.

About Podean

Menu

Latest Posts

Skai Director of Sales joins Podean as Director of Retail Media Partnerships

September 12, 2023

Comments are closed.